Last March, the un-elected Atlantic County Improvement Authority agreed to borrow $97 million to build a private water park next to the Showboat in Atlantic City. It will be owned by Bart Blatstein. Blatstein is a Philadelphia developer who owns Showboat in Atlantic City as a non-casino hotel. Blatstein also owns several projects in Philadelphia. Several years ago, he was unsuccessful in trying to revive the failing Ocean One Pier across the Boardwalk from Caesars in Atlantic City.

Shortly afterwards, the Improvement Authority approved the loan, the governing body of Atlantic County (Board of Commissioners, formerly Freeholders) also approved it. They did so after being told that Atlantic County taxpayers could not be held responsible if the project failed. Although that is technically and legally correct, taxpayers are almost always forced to bail out failed projects, even when they have no legal obligation to do so.

The bonds in question are “revenue bonds”. A “revenue bond” is a debt paid back with income from a specific project. It is different from a much more secure “general obligation bond”. General obligation bonds force state and local governments to pay back loans by raising real estate taxes even when a project fails to earn enough money.

However, when a “revenue bond” project fails, it ruins the credit ratings of every government agency in the state. Often financial “experts” warn that bond defaults by government agencies will trigger a “financial crisis”. As a result, New Jersey taxpayers routinely bail out insolvent agencies that default on their “revenue bonds”, even when there is no legal obligation to do so. In 1992, Republican Governor Christie Todd Whitman bullied Atlantic County into bailing out its Utilities Authority. The Atlantic County Utilities Authority had used “revenue bonds” to borrow $82 million to build a trash incinerator that was supposed to pay for itself. Somehow, the $82 million was spent and the incinerator was never built. Five years ago, Republican Governor Chris Christie and a Democrat State Senate and Assembly bailed out “revenue bonds” of the insolvent NJ Transportation Trust Fund Authority even though they had no legal obligation to do so. They did it by giving us hikes in tolls and gasoline taxes almost every year since 2016.

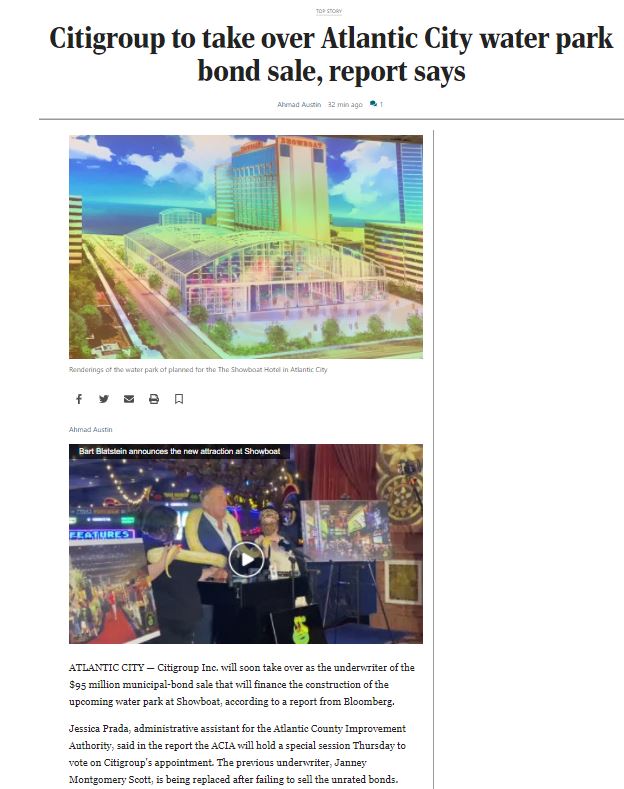

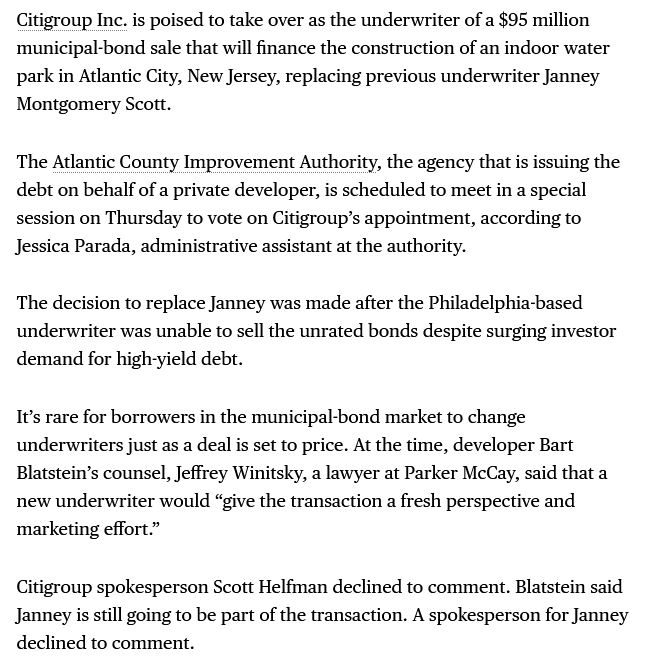

Last March, the Atlantic County Improvement Authority hired the Wall Street investment bank Janney Montgomery Scott to borrow the money by selling $95 million in “revenue bonds”. Earlier this month, Bloomberg.com reported that Janney was unable to find investors to buy those bonds. Last Monday, Bloomberg reported that the Authority planned to have Citigroup Inc. take over the deal.

Excerpt from article posted by Bloomberg.com on July 26, 2021. Click here for link to full post.

According to Bloomberg.com, these “revenue bonds” were “unrated” but paid a high rate of interest. Wall Street investors are usually offered extra high interest when there is extra high risk that bonds from a troubled private corporation or “revenue bonds” from a government agency might not be paid back and lose most or all of their value. Wall Street investors commonly describe these bonds as “junk”. The Bloomberg article reported that these Blatstein Water Park bonds failed to sell “despite surging investor demand for high yield debt” elsewhere.

Yesterday, the Atlantic County Improvement Authority announced it is having a special public meeting this Thursday. They say they plan to replace Janney Montgomery Scott with a new investment bank, Citigroup, Inc. to sell the bonds. According to Bloomberg, “It is rare for borrowers in the municipal-bond market to change underwriters just as a deal is set to price”. Bart Blatstein said Janney would still be part of the transaction. Blatstein’s lawyer, Jeffrey Winitsky said a new underwriter would “give the transaction a fresh perspective and marketing effort”. However spokespersons for Janney and Citigroup declined to comment to Bloomberg.

It also seems unusual that the Authority is not doing any investigation or holding any public hearings on why Wall Street Investors did not want to lend money to this project. If they think the project is too risky for them, should we ask if it is too risky for Atlantic County taxpayers? Is this a sound project? Or is this to reward Blatstein for bailing out Stockton University. In 2014, Stockton University spent $18 million to buy the Showboat Casino when it closed, but was unable to use it because of a restrictive covenant. However, one year later, Blatstein rescued Stockton by paying it $22 million for the building.

It is worth mentioning that proposals to build a waterpark at the abandoned Atlantic Palace Casino at Boston Avenue and the Boardwalk (Steve Wynn’s original Golden Nugget) failed because they could not find enough lenders or investors in 2015, and again in 2017.. What makes this water park project better?

But what will Citicorp do to sell this “junk” that Janny Montgomery Scott could not do? The failed Revel Casino comes to mind. In 2011 Republican Governor Chris Christie and top Democratic leaders in the legislature agreed to support a $1.15 billion loan package to complete the Revel Casino project after the Wall Street firm Morgan Stanley abandoned it. Private investors would loan $850 million, which would be secured by the completed building. New Jersey’s “Economic Development Authority” would sell “mezzanine bonds” to borrow the other $350 million which would be secured by nothing! The Revel Casino was completed and opened in 2012. It was a complete flop and closed two years later. It was sold to Florida developer Glen Straub for $82 million in 2015.

That means “secured” investors who loaned the $850 million got less than nine cents back on every dollar they invested. Those who bought “mezzanine bonds” got nothing. Who lost more than a billion dollars in just two years? Why didn’t any of them sue the banks or brokers who sold them this junk? Why didn’t any of them even publicly complain about their colossal losses?

Later we learned that several hedge funds operating out of Morris County, invested in these Revel bonds. We also later learned that administrators of New Jersey’s public employee pension funds had given these hedge funds hundreds of millions of dollars to invest. We also remember that at least one Republican Governor of a another state publicly complained that our Governor Chris Christie had persuaded him to invest some of his state’s pension money in Revel Casino bonds. Is Citicorp being selected because it has more political juice than Janney? Will Citicorp “persuade” pension fund administrators to invest in Blatstein’s Water Park bonds?

The Atlantic County Improvement Authority will hold a special meeting at 10 AM this Thursday, July 29, 2021. If they decide to switch to Citicorp and go through with the project, the Atlantic County “Commissioners” (formerly Freeholders) will meet to decide if they should approve the modified plan. The public will only be allowed to participate online via Zoom. Below are the links and log-in information for the meeting.

Zoom Meeting Time: July 29th, 2021, 10:00 AM Eastern Time (US and Canada)

Join Zoom Meeting at the following link:

https://zoom.us/j/97139112249?pwd=ek1EUTlBVzZzY0kwWXBUMGtzV3Zkdz09

Or Dial by your location +1 929 205 6099 US (New York)

Meeting ID: 971 3911 2249

Passcode (if needed): 539221

THIS ISSUE MAY HAVE NATIONAL AND INTERNATIONAL IMPORTANCE. HERE’S WHY:

Many economists think the United States and the world are facing a massive economic collapse. However, they strongly disagree how it will happen. Most say it will come from “hyperinflation”. They say that for the past twelve years, the United States recklessly spent trillions of dollars more than it collected in taxes. To pay for this, our government has printed trillions of dollars of paper money with nothing of value to back it up. It has even issued trillions of electronic dollars. As a result people are demanding more of these dollars for everything we buy. This is what happened in Germany during the early 1920s and in Zimbabwe (Rhodesia) fifteen years ago. In both countries, it took millions, and later billions of German marks and Zimbabwe dollars to buy a loaf of bread or gallon of milk. Prices went up so fast that people rushed to buy something with their paper money as soon as they got it. That was because they knew their paper money would by less a few hours later. Financial planners who believe “hyperinflation” is coming are urging their clients to borrow money. They way anyone who borrows money today can pay back the loan with much cheaper dollars in future years.

However, other economists predict our economy will collapse from massive “deflation”. One of them is Rick Ackerman. Ackerman grew up in Margate and is a 1967 graduate of Atlantic City High School. He began his career as a reporter for the Press of Atlantic City. He then moved to San Francisco where he was a floor trader and options dealer on the Pacific Stock Exchange for many years. Today, he is a trader and “chartist”. He publishes “Rick’s Picks”, a financial newsletter. He also teaches his “hidden pivot” method for analyzing investment trends. Here is an excerpt from his latest post on the subject. Click here for his full post at Rick’s Picks – Rick Ackermen – Ricks Picks (rickackerman.com).

“Predictions of massive “hyperinflation” flatly contradicts a forecast I’ve held to for decades – i.e., that deflation would ultimately wreck the global economy, driving the dollar into such scarcity that many, if not most, Americans will have to barter to survive. This may seem hard to believe at the moment, given the Fed’s reckless monetary blowout and the illusory prosperity it has created. Most of the virtual money has gone into investable assets, triggering a historical run-up in stocks during a year of Covid lockdowns. It has also created a real estate bubble even more extreme than the one that popped in 2008, nearly taking the global economy with it.

This Isn’t the 1970s

“We should note that the current inflation is very different from the one of the 1970s. That was self-perpetuating to the extent wages and prices drove each other higher in a seemingly endless spiral. The current inflation is not self-perpetuating; rather, it is being driven by an increase in paper wealth that will reverse and crash in the next bear market. Nor are people desperate to trade dollars for physical assets, as occurs in a hyperinflation; mainly, it has been Baby boomers spending a significant portion of their paper wealth on second homes in desirable locations away from urban centers.

“Still, one might ask: With the Fed and every other central bank inflating like there’s no tomorrow, how could deflation possibly result? The answer lies in the inescapable fact that every penny of what we collectively owe must ultimately be repaid –if not by the borrower, then by the lender. This implies, for one, that when Biden and the Democrats “forgive” student loans amounting to $1.7 trillion, creditors will eat the entire loss. Twelve zeroes worth of receivables will be wiped from their books with the stroke of the President’s pen; shortly thereafter, yacht prices will begin to soften in West Palm Beach, and the market for $20+ million homes in the Hamptons will appear to totter, producing tremors in Aspen, Scarsdale and Atherton.

“Now imagine this implosion multiplied a hundredfold. That’s what will happen when the inevitable bear market in stocks unfolds. It will suck many more digital dollars into a black hole of deflation than the Fed could conceivably monetize in an unrehearsed attempt to hold off a collapse. The deleveraging will not stop until it has reduced the $2 quadrillion financial derivatives market to an infinitely dense singularity. A thousand financiers working 24/7 and backed by the full faith and credit of the U.S. Government will not be able to pry loose even a dime of credit from that market for at least a decade. That’s how long it will take, at a minimum, for a wrecked middle class to push their credit scores back above 400.

Dollar Short-Squeeze

“The collapse will end our misplaced faith in a bank clearing system that is as fragile as Delft pottery, rendering ATMs and credit cards useless overnight. Money markets will seize up as lenders refuse to roll overnight loans, instead demanding settlement in cash. That’s when we will discover that real cash-dollars are actually in short supply. In the absence of a functioning market for digital dollars, the resulting short-squeeze on real ones will be like the one that pushed the shares of Gamestop and AMC into the stratosphere. The comparison is appropriate because, like debt issued by those two companies, the dollar ultimately is just a worthless I.O.U.

“For the time being, however, the dollar will remain under pressure despite assurances from Fed bag-man Jerome Powell that inflation has peaked. We should note, however, that the dollar has not exactly collapsed under the weight of wantonly reckless Fed stimulus. To the contrary, and as the chart above makes clear, the greenback is down just 4% from the sweet spot of its pre-pandemic trading range. Moreover, a key, long-term support at 90 has survived two brutal shakedowns this year. Although the support could conceivably give way on renewed selling, nothing in the chart says this is likely, let alone that the dollar is in a condition of imminent collapse. . . ”

The proposed Atlantic County Authority “revenue bonds” for Blatstein’s Water Park is a perfect example of Rick Ackerman’s theory. Investors who buy $95 million of those bonds will at first appear to be very wealthy. They will be receiving very high interest on those bonds every three months. Because they will have high income, they will spend freely and drive up the prices of everything they buy. However, if the project fails and they lose their entire investment, they will be broke. Especially if they stop getting monthly payments from insolvent pensions, and lose money on other investments. If they and everyone else who is suddenly broke are unable to buy anything or even go out to restaurants, prices will fall as “deflation” sets in.

Finally, both New Jersey and America have been here before. It 1837, there was a devastating six year economic collapse that threatened the survival of America. It was caused by state and local government borrowing massive amounts of money to build roads, canals, and other projects that failed to produce enough money to pay back the loans. Much of this was because of “systemic corruption” in state and local government. Because many banks invested in state and local bonds issued to pay for these projects, they failed when these bonds became worthless. Anyone who kept their savings in those banks lost everything. New Jersey and most other states responded to this disaster by adopting new state constitutions. These new constitutions made it very difficult for state and local governments to borrow money. They were so successful that until 1960, New Jersey state government was virtually debt free. All that changed in the 1960’s. That was when the New Jersey Supreme Court created loopholes in our state constitution. It allowed state and local government to set up independent “authorities” and other gimmicks to borrow money for pet projects indirectly. Click here for details on how and when this happened.

We are a group of roughly 200 citizens who mostly live near Atlantic City, New Jersey. We volunteer our time and money to maintain this website. We do our best to post accurate information. However, we admit we make mistakes from time to time. If you see any mistakes or inaccurate, misleading, outdated, or incomplete information in this or any of our posts, please let us know. We will do our best to correct the problem as soon as possible.

Also, because Facebook, Twitter, and other social media platforms falsely claim our posts violate their “community standards”, they greatly restrict, “throttle back” or “shadow ban” our posts. Please help us overcome that by sharing our posts wherever you can, as often as you can. Please click the social share links below. Also copy and paste the link to the “comments” section of your favorite sites like Patch.com or PressofAtlanticCity.com and email them to your friends. Thanks.

Seth Grossman, Executive Director

LibertyAndProsperity.com

(609) 927-7333