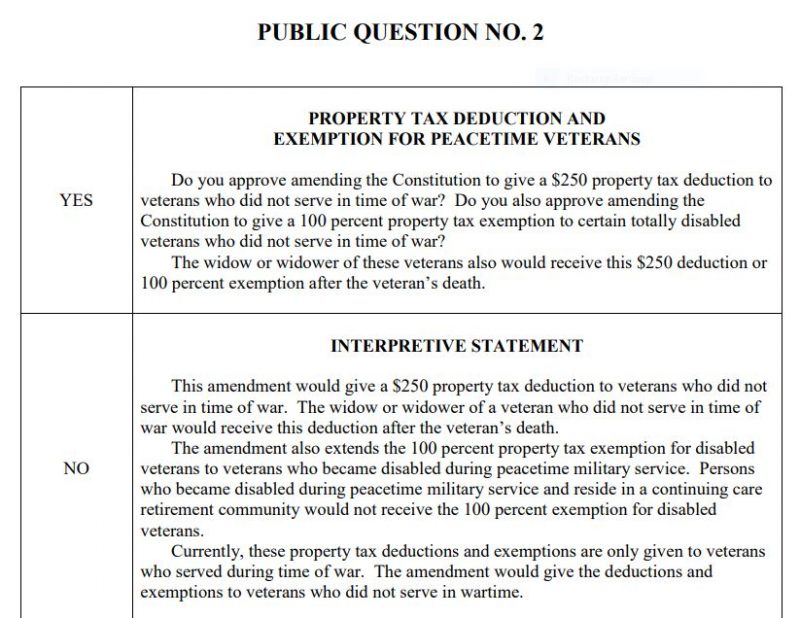

This is the only information so far given to voters about this proposed amendment to the NJ State Constitution. Once amended, the State Constitution is almost impossible to change. So far, the below “Fiscal Estimate” showing huge impact on property tax bills is not well known. Please read it before voting.

This “Fiscal Estimate” was prepared by the Office of Legislative Services last January on the same day that Legislators voted on the measure. Click here for the link to that report, which is copied below:

https://www.njleg.state.nj.us/2018/Bills/ACR/253_E1.HTM

The OLS “Fiscal Estimate” below states that it understates the full cost of the measure, because Governor Murphy’s administration did not provide data needed to estimate the cost of benefits to surviving spouses.

There are two property tax deductions now available to veterans who served during wartime or declared “national emergency”. One is the $250 property tax deduction for all honorably discharged veterans and their surviving spouses. The second is a 100% property tax exemption available to all veterans who are “totally disabled”. (The state deems veterans declared 60% disabled by the federal VA to be “totally disabled”)

The OLS estimates that roughly 52,834 new peacetime non-disabled veterans will qualify for the $250 per year deduction. This will cost roughly $13 million each year, and will be paid from existing state income tax property tax relief funds. That will leave less money for state aid to public schools and rebates for other homeowners. The OLS did not estimate the additional cost of paying this benefit to surviving spouses of non-disabled peacetime veterans.

The OLS report estimates that approximately 4,340 new peacetime veterans with a service related disability will qualify for full property tax exemption on their homes. (New Jersey has a practice of deeming veterans declared 60% disabled by the Federal VA to be 100% “totally” disabled” to qualify for the state exemption. The OLS estimates that this new exemption will cost taxpayers in the towns where these veterans reside $38 million. That money come from property tax increases on all other property owners. The OLS stated it did not have sufficient data to estimate the cost of giving that benefit to surviving spouses of those veterans.

LEGISLATIVE FISCAL ESTIMATE

ASSEMBLY CONCURRENT RESOLUTION No. 253

STATE OF NEW JERSEY

218th LEGISLATURE

DATED: JANUARY 14, 2020

| Synopsis: | Proposes constitutional amendment to extend veterans’ property tax deduction and veterans’ property tax exemption to certain veterans who did not serve in time of war or other emergency. |

| Type of Impact: | Increase in State expenditures from the Property Tax Relief Fund; Increase in municipal revenues; potential increase in municipal expenditures |

| Agencies Affected: | Department of the Treasury and municipalities. |

| Office of Legislative Services Estimate | |||||

| Fiscal Impact | Year 1 | Year 2 | Year 3 | ||

| State Cost Increase | $13.6 million | $13.0 million | $12.4 million | ||

| Local Revenue Increase | $266,000 | $254,000 | $243,000 | ||

| Potential Local Expenditure Increase | Indeterminate | ||||

- The Office of Legislative Services (OLS) estimates that the constitutional amendment would result in an annual increase in State expenditures associated with the provision of property tax deductions to peacetime veterans who did not serve during a time of war or other emergency.

- Using information from the United States Department of Veterans Affairs and the Department of Community Affairs, it is estimated 53,274 peacetime veterans will qualify for the property tax deduction in Tax Year (TY) 2020. Assuming that each veteran receives the full deduction, the State would be expected to incur an additional cost of approximately $13.6 million for TY 2020 as a result of the constitutional amendment. Due to an estimated decline in the population of veterans over time, this State expenditure is expected to decrease to approximately $13.0 million in TY 2021 and $12.4 million in TY 2022.

- Municipal revenues are expected to increase by approximately $266,000 in TY 2020 and decline slightly thereafter from the receipt of State funds equal to $5 for each beneficiary claiming the property tax deduction, with the funds intended to offset increased administrative expenses. This amount assumes all eligible veterans claim the deduction.

- The constitutional amendment also expands eligibility for the disabled veterans’ property tax exemption to include certain peacetime veterans. Using information from the United States Department of Veterans Affairs and the State Department of the Treasury for 2018, the constitutional amendment will shift approximately $38 million of the State-wide property tax levy to non-exempt taxpayers. Therefore, local government revenues are not expected to decrease as a result of this constitutional amendment.

- There is the potential for an increase in municipal expenditures for administrative costs associated with the expansion of the property tax deduction and exemption to include additional beneficiaries. The extent of this increase will depend on the operations of each municipality.

BILL DESCRIPTION

If approved by the voters of the State, this proposed constitutional amendment would make honorably discharged military veterans who did not serve during time of war or other emergency eligible for the $250 property tax deduction and the property tax exemption granted by law to veterans with a service-connected disability. Currently, these property tax benefits are given only to honorably discharged military veterans who served during time of war or other emergency.

FISCAL ANALYSIS/EXECUTIVE BRANCH: None received.

OFFICE OF LEGISLATIVE SERVICES

The OLS estimates that the constitutional amendment would result in an annual increase in State expenditures associated with the provision of property tax deductions to veterans who did not serve during a time of war or other emergency. This increase in State expenditures in TY 2020 is estimated to be $13.6 million. The constitutional amendment also expands eligibility for the disabled veterans’ property tax exemption to include totally disabled peacetime veterans. Using information from the United States Department of Veterans Affairs and the State Department of the Treasury for 2018, the constitutional amendment will redistribute approximately $38 million of the State-wide property tax levy to non-exempt taxpayers.

Veterans’ Property Tax Deduction

Under current law, a person who was honorably discharged after serving in any branch of the Armed Forces of the United States during a time of war or other emergency, and the surviving spouse of any such veteran, is entitled to receive an annual $250 property tax deduction. Continuing care retirement communities also receive the property tax deduction on behalf of each eligible veteran that resides in the facility. A municipality applies the property tax deduction to each beneficiary’s tax bill and the State is required to reimburse the municipality in an amount equal to 102 percent of the total amount of property tax deductions provided in that municipality. The State reimbursement for the maximum property tax deduction of $250 would therefore equal $255.

The constitutional amendment provides that every honorably discharged veteran would be entitled to receive the property tax deduction, regardless of whether that veteran served during a time of war or other emergency. Consequently, the constitutional amendment would increase State expenditures associated with the reimbursement of every property tax deduction that is provided to a peacetime veteran. This expenditure increase would be equal to: (1) the number of (i) property-owning peacetime veterans, and (ii) peacetime veterans who reside in a continuing care retirement community; multiplied by (2) the State reimbursement, which may not exceed $255 for each property tax deduction.

According to information published by the United States Department of Veterans Affairs, approximately 82,553 peacetime veterans, including homeowners and renters, are expected to reside in New Jersey by 2020. The department further projects that the population of peacetime veterans in this State will be 78,719 in 2021 and 75,225 in 2022. Information from the United States Census Bureau indicates that the average homeownership rate in this State is 64 percent.

Using this information, the OLS estimates that approximately 52,834 property-owning peacetime veterans would become eligible for the veterans’ property tax deduction in TY 2020. Assuming that each of these veterans will be credited with the full $250 property tax deduction, the State is expected to incur an additional cost of approximately $13.5 million associated with the reimbursement of TY 2020 property tax deductions for property-owning peacetime veterans. Thereafter, these additional costs are expected to decrease to approximately $12.8 million in TY 2021 and $12.3 million in TY 2022, reflecting the decrease in the population of peacetime veterans in the State.

According to information provided by the Department of Community Affairs in 2018, the total occupancy of all continuing care retirement communities in the State was 9,835 persons. Information from the United State Census Bureau and the department, respectively, indicates that: (1) approximately 16.9 percent of State residents over the age of 65 years are veterans; and (2) approximately 26.5 percent of all veterans in the State served during peacetime. Using this information, the OLS estimates that approximately 440 peacetime veterans reside in continuing care retirement communities. Assuming that each veteran is credited with the full $250 property tax deduction, the State is expected to incur an additional annual cost of approximately $112,200 associated with the reimbursement of property tax deductions for peacetime veterans who reside in continuing care retirement communities.

Consequently, the OLS estimates that the constitutional amendment would increase State expenditures by approximately $13.6 million associated with the reimbursement of municipalities for TY 2020 property tax deductions, including the $5 per beneficiary administrative payment. Thereafter, the fiscal impact of the constitutional amendment is expected to equal $13 million in TY 2021 and $12.4 million in TY 2022. Municipal revenues are expected to increase by approximately $266,000, $254,000, and $243,000, respectively, during these three years from the receipt of these State funds, assuming that each eligible veteran claims the deduction.

The OLS notes that the constitutional amendment also allows the surviving spouses of these peacetime veterans to receive the property tax deduction. Due to information constraints, the OLS is unable to determine the number of surviving spouses that may also qualify for the property tax deduction.

Disabled Veterans’ Property Tax Exemption

As permitted under the State Constitution, current law provides a 100 percent property tax exemption for certain veterans, and the surviving spouses thereof, who: (1) were honorably discharged after serving in any branch of the Armed Forces of the United States during a time of war or other emergency; (2) suffer from a service-connected disability that was declared by the department to be a total or 100 percent permanent disability; and (3) do not reside in continuing care retirement communities or other rental premises. According to the New Jersey Department of Military and Veterans Affairs, a veteran with a disability rating of at least 60 percent, and who is declared “individually unemployable,” is considered to be 100 percent permanently and totally disabled for the purposes of the property tax exemption.

The constitutional amendment would increase eligibility for the disabled veterans’ property tax exemption to include those veterans that did not serve during a time of war or other emergency, and their surviving spouses. The OLS expects the cost of these additional property tax exemptions to be absorbed by other property taxpayers within each municipality.

According to information published by the department, 25,590 veterans in this State were declared to have a service-connected disability rating of 70 percent or more in 2018. However, due to information constraints, the OLS is unable to identify: (1) the number of veterans with a disability rating between 60 percent and 70 percent; and (2) the number of surviving spouses of any disabled veterans. In 2018, the department estimates that approximately 26.5 percent of all veterans in New Jersey served during peacetime.

Based on this information, the OLS estimates that approximately 6,781 totally disabled peacetime veterans resided in the State in 2018, assuming that every veteran with a disability rating of 70 percent or greater, but less than 100 percent, was declared “individually unemployable.” Using the average homeownership rate in this State of 64 percent, the OLS further estimates that approximately 4,340 totally disabled peacetime veterans paid property taxes in 2018.

Assuming that each of these veterans paid the average Statewide property tax of $8,767 during that year, the provisions of this constitutional amendment would have resulted in the exemption of approximately $38 million in additional property tax payments in 2018. However, as noted, this estimate does not include the property tax exemptions that would have been provided to the surviving spouses of totally disabled peacetime veterans and those qualified peacetime veterans with a disability rating between 60 percent and 70 percent.

Consequently, the OLS notes that the constitutional amendment will shift the annual property tax levy by approximately $38 million (based on information for 2018), which will be redistributed to other non-exempt taxpayers. Given that the fiscal impact of the disabled veterans’ property tax exemption is redistributed to other non-exempt taxpayers, local government revenues are not expected to decrease as a result of the constitutional amendment. However, there is the potential for an increase in municipal expenditures for the administrative costs associated with the expansion of the property tax deduction and exemption to include additional beneficiaries. The extent of this increase will depend on the operations of each municipality.

| Section: | Local Government |

| Analyst: | Joseph A. Pezzulo

Associate Research Analyst |

| Approved: | Frank W. Haines III

Legislative Budget and Finance Officer |

This legislative fiscal estimate has been produced by the Office of Legislative Services due to the failure of the Executive Branch to respond to our request for a fiscal note.

This fiscal estimate has been prepared pursuant to P.L.1980, c.67 (C.52:13B-6 et seq.).